How Much Super Do I Need to Retire in Australia?

We all get to that point where we decide that we no longer want to do the day-to-day work thing and wish it was our first day of retirement. No alarm, no commute, no inbox full of urgent emails or tasks that must be done. Just a quiet morning and the comforting feeling that your time finally belongs to you.

But before we get to this glorious morning, we need to ask the question “How much super do I need to retire?” That’s where a super financial advisor can help.

It’s one of the most common, and most overwhelming, questions in our mid to later years. There’s no single magic number, and the internet certainly hasn’t helped by throwing around everything from $300,000 to $1.5 million like it’s pretend money. The truth is simpler and more personal – the amount you need depends on your life, your habits, your dreams, and how you want to spend those long, alarm-free days.

We will break down what really matters when calculating your retirement number, without the jargon, guesswork, or financial guilt trips.

Let’s make this easier.

Most people hugely overestimate or underestimate what they need to retire and the numbers they believe are surprisingly consistent across multiple surveys.

What people think they need

Most Australians believe they need around $1 million to retire comfortably. This number pops up again and again because it sounds like a safe round figure, not because it’s actually personalised.

What people fear they need

A growing number, especially younger Australians, believe they’ll need $2–3 million due to rising costs, longer lifespans, and scary media headlines about the cost of living. Keep in mind that younger Australians will have also had access to a higher rate of compulsory super for a longer period of their working lives than many retirees or those close to retiring have had.

Where these beliefs come from

- The media loves the “$1 million for retirement” line.

- People assume they’ll need to fully self-fund 25–30 years without help.

- Many don’t realise the Age Pension can play a major role.

- The idea of “never outliving your money” makes them aim high to feel safe.

Reality check

Most Australians who are actually retired do not have anything close to $1 million—and many live comfortably with:

- a modest super balance

- lower expenses after work

- the Age Pension supplementing income

What You Actually Need Depends on Your Lifestyle which most people find both surprising and liberating as your retirement number isn’t universal, it’s personal.

Two people can retire with the same balance and have completely different experiences, simply because their lifestyles are different. Being a super financial advisor we can help you achieve your retirement goals.

Think of it like planning a holiday.

You can go to the same destination as someone else, but your budget depends on how you travel:

- Do you like nice restaurants or prefer home-cooked meals?

- Are you dreaming of caravanning around Australia, or are you happiest pottering around the garden?

- Do you own your home, or do you plan on downsizing/buying a home or continue to rent?

- Do you want to travel overseas every year, or is visiting family within Australia enough?

This is why the idea of “everyone needs $1 million” falls apart. Some people genuinely do need that much or more. Others can retire comfortably on far less, especially if the Age Pension will play a role.

A simple way to think about it

Instead of obsessing over a lump sum, think about:

- How much you want to spend each year in retirement

- How much will come from super, investments, or savings

- How much the Age Pension could top up

Once you know your lifestyle costs, the maths becomes much clearer — and far less intimidating. Most people discover they need less than the scary numbers they’ve been hearing. Read our blog post to learn more about how a financial planner can help manage your super.

A Quick Formula to Estimate Your Retirement Number

If you want a simple, no-maths-degree way to work out your retirement number calculation , here’s an easy formula used by financial planners around the world:

Step 1: Work out how much you want to spend each year

This is your lifestyle number — not a guess, but a realistic estimate of your budget. I often say that this word is a “swear word” as many clients avoid ever going near a budget.

For most Australians, a comfortable retirement often sits between $50,000–$75,000 per year for a couple, and $42,000–$55,000 for a single. This does not include big trips, but the everyday things as well as some activities.

Step 2: Subtract any Age Pension you may expect to receive

Most Australians qualify for at least a **part Age Pension** at some point. This reduces how much you personally need to fund.

For example:

If you expect to spend $60,000 per year and receive $25,000 in Age Pension, your investments only need to provide $35,000 per year.

Step 3: Multiply the result by 25

This is a widely used guide called the “25x rule.”

It estimates the size of a nest egg that can sustainably support withdrawals over a long retirement, preferably a 25 year long lifespan in retirement.

Retirement savings needed ≈ (Annual spending you need to fund) × 25

Example

- Desired spending: $60,000 per year

- Age Pension: $25,000 per year

- Amount you must self-fund: $35,000 per year

$35,000 × 25 = $875,000 required in super/savings

Not a perfect formula—but it instantly turns vague theory into a tangible, realistic number you can work with. Check out our blog on how much money to save to retire.

This formula often works because it builds on the idea that:

- your investments will keep earning returns even after you retire

- your spending often decreases as you age

- the Age Pension acts as a long-term stabiliser

Comfortable retirement superannuation balances

1. Your expenses usually drop in retirement

Most retirees spend less than they did while working because:

- There’s no commuting, parking fees, work wardrobe or lunches out

- The mortgage is often paid off

- Kids are financially independent

- You finally have time to shop smarter and cook at home

Even big expenses like travel tend to taper off as people move into their later 70s and 80s.

2. The Age Pension acts as a long-term safety net

Even if you don’t qualify for the Age Pension immediately, many people become eligible later as their super reduces. This means you often don’t have to fully self-fund 25–30 years of expenses.

3. You don’t spend evenly throughout retirement

Retirement spending typically follows the “go-go, slow-go, no-go” pattern:

- Go-go years (60s–early 70s): You’re active, travelling, dining out.

- Slow-go years (mid-70s–late 80s): You still enjoy life, but activity slows and spending drops.

- No-go years (late 80s–90s): You’re at home more, with lower lifestyle spending (but possibly higher health costs).

Most people fear they’ll spend like a 65-year-old forever — they won’t.

4. Super keeps working even after you retire

Your investments don’t stop earning just because you’ve stopped working. Returns, dividends, and growth mean your money continues to support you, extending how long your balance lasts.

5. You don’t need your starting balance to cover your full lifespan

People often think all the money they’ll ever need must be sitting in their super on day one.

In reality:

- your balance declines gradually

- the Age Pension gradually increases as your assets fall

- withdrawal rates adjust as your spending changes

It’s a dynamic system — not a one-off lump sum.

Learn more about how to plan for retirement in Australia.

Here are some real examples:

Jane has been living with her father for many years as his career as well as working fulltime. He recently passed and his estate has been wound up. Jane needs to find somewhere new to live as she didn’t want to buy their former home. It’s a great “first home buyers’ cottage” that needs a modern renovation that she just does not want to do.

As Jane was not paying rent, but was contributing to other household expenses, she had capacity to add funds into her super account along the way and at age 64 has a really healthy balance.

Jane is going to purchase a brand-new unit in an over 55’s village. She feels that she will make friends, have safety and people to watch her unit if she goes away. The unit is not quite ready yet, so she gets to pay it in 2 parts.

There are several moving parts to this strategy for Jane.

- The initial deposit of $100,000 has been paid with some cash she had saved as well as a lump sum from her super as part of a transition to retirement strategy (TRIS).

- The rest of the payment will be sourced from her super after she turns age 65 and has full access to her super.

- Jane completed the dreaded “b” word – a budget – and is very confident that she will have sufficient funds, even with the ongoing costs in a village to continue to have a comfortable lifestyle.

- Jane will remain working in the meantime and continue to salary sacrifice her surplus funds to rebuild her super with an aim to retire at age 67. She really likes her job and is happy to stay there a couple years longer.

- Jane’s estimated living expenses are quite low as she likes to stay about the home, travel local and already has furniture etc for her new home.

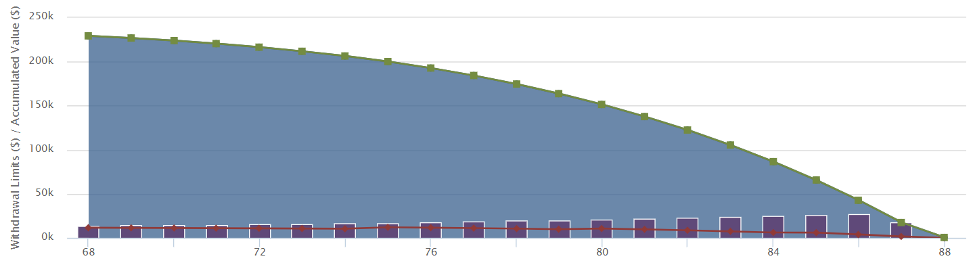

- With a new estimated super balance of approx. $240,000 and factoring in CPI, it is anticipated Jane’s pension balance will assist to meet her living expense requirements for a comfortable retirement up to around aged 87.

- She will also qualify for the full aged pension and will now own her own home.

Jane did not think that a $240,000 balance would be sufficient for her and thought she would have to keep working for much longer.

Projection of Account Based Pension Investment and Income Limits – Jane

A real example for a couple

John and Lily have been going through some tough business times, had accumulated debts including with the ATO and had issues with a tenant in their investment property that they bought in a suburb that has stalled. They have a self managed super fund that also had issues with the property due to cladding problems on the exterior and needing to spend money and not have a tenant for a very long time. They are over age 65 but were still working as they did not have sufficient cash flow to not work. They had very little super, being self-employed this is not unusual.

Several strategies were needed for this lovely couple.

- Investment property was vacant so time to prep it and sell it. Its value hadn’t changed much since they bought it 4 years ago, so minimal capital gains to worry about after deductions etc.

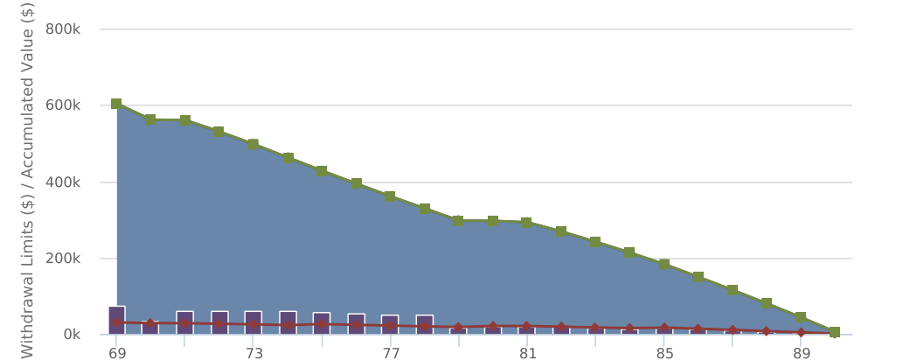

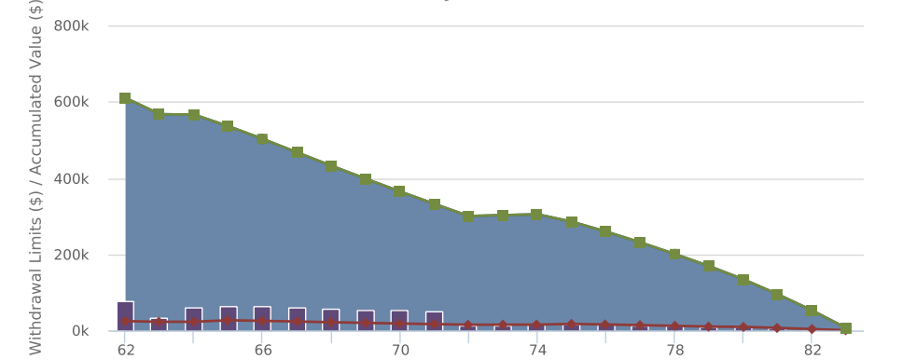

- The sale of the property allowed them to clear all debt of approx. $255,000 and walk away with $760,000 that they can add into their superannuation this year.

- The SMSF will be retained until the commercial property cladding issue is resolved and then wound up. Funds can then be added to their pensions as part of a refresh.

- By adding available cash into a new pension fund, they can commence drawing down a tax free income for their comfortable retirement requirements and have their first relaxing trip in a really long time.

- The graphs below show that their super funds will last well into the 80’s, with Centrelink Aged Pension kicking in at a later date for them giving them further funds for their needs in the future.

John and Lily were very worried about their lack of super balance, properties that turned out to be not such great investments and thought there was no end in sight for their retirement. They felt very trapped. Whilst a $1.2m balance is large and more than many people have access to, it was really hard fought for them to get there.

Projection of Account Based Pension Investment and Income Limits – Lily

Projection of Account Based Pension Investment and Income Limits – John

FAQ: How Much Do I Need to Retire at 60?

1. Is retiring at 60 realistic in Australia?

Yes – but it depends on your super balance, lifestyle expectations, and whether you’re prepared to bridge the gap before Age Pension age (67). Many people retire at 60 using a Transition to Retirement strategy, account-based pensions, or part-time work.

2. How much do most people actually retire with at 60?

Most Australians retiring at 60 have far less than the “$1 million” figure. Many have between $200,000–$600,000 in super, and adjust their lifestyle, work part-time, or draw on savings to make it work.

3. So how much should I have by age 60?

A general guide for a comfortable lifestyle at 60 is:

- Singles: around $250,000–$600,000

- Couples: around $500,000–$1 million

But this varies massively based on spending, debts, and whether you’ll get the Age Pension in the future.

4. Does retiring at 60 mean I’ll run out of money earlier?

Not automatically. Your super keeps earning returns, and your spending usually reduces over time. You may also become eligible for the Age Pension later, which helps stretch your savings. But it is something that you need to think carefully about and receive advice on.

5. How do I cover the gap from 60 to 67 (Age Pension age)?

Options include:

- drawing from your super via an account-based pension

- working part-time

- using savings or investments

- downsizing your property

- using your partner’s income or super if you’re a couple

Good planning can make these years very manageable.

6. What’s the minimum amount needed to retire at 60?

There’s no strict minimum. People have retired with as little as $200,000–$300,000, especially if:

- they’re mortgage-free

- they live modestly

- they expect to qualify for the Age Pension at 67

- they’re comfortable with a simpler lifestyle

7. How much income do I need each year in retirement?

Typical spending ranges are:

- Singles: $42,000–$55,000 per year

- Couples: $50,000–$75,000 per year

Your personal lifestyle could be above or below this.

8. What if I’m not on track by 60?

You still have options:

- delay full retirement a couple of years

- work part-time

- boost super with catch-up contributions

- invest outside of super

- downsize the home

- adjust your lifestyle goals

- manage your super funds – review your current funds for fees and make sure you only have 1 where possible.

You don’t need a perfect plan — just a flexible one.

9. Does retiring at 60 affect my super tax treatment?

Once you’ve reached preservation age (58–60 depending on your birth year), you can access your super tax-free if you retire. Any pension income you draw is also tax-free after 60.

10. How do I calculate my own retirement number at 60?

A quick formula is:

(Annual spending you want – Age Pension you expect) × 25

This gives you a rough lump sum target.

The key takeaway

The gap between what people think they need and what they actually need is huge.

The real number depends on lifestyle, assets, Age Pension eligibility, and spending—not a magic round number.