Financial Advisor Cost in Australia for 2026

The cost for hiring a financial advisor in 2026 generally starts at about $4,000 to $5,000 per year for ongoing support. If you are looking for a comprehensive initial financial plan, prices typically range between $5,000 and $12,000, depending on the level of work that is required. *

While these costs have increased due to higher professional standards, the right advisor can help you find significant savings through tax strategies and superannuation rules.

In this article, we’ll break down the different fee structures and key factors to consider when choosing a financial advisor.

What Are The Different Types of Financial advisor Fees?

There are a few different ways financial advisors charge, each with its own factors to consider.

Asset based

Asset-based fees are less common today but are still used by some financial advisors. This fee structure charges a percentage of the total assets under management (typically 0.5%–2%). The idea is that it pushes advisors to grow your portfolio since their earnings increase as your assets grow. However, in some cases, advisors may receive high fees without actively growing the assets or providing value.

Hourly

Charging by the hour is usually reserved for one-off meetings or for specific technical tasks. In 2026, hourly rates for a senior advisor often fall between $330 and $650 per hour. This method can be hard to predict if your situation requires more time than was first expected.

Commission Based Fees

Under the Delivering Better Financial Outcomes (DBFO) rules, advisors do not receive commissions on investment products. They can still receive them for insurance products, but as of 2026, they must get your explicit written consent before they accept any payment from an insurer. This makes sure that you are fully aware of what is being paid.

Flat Fees

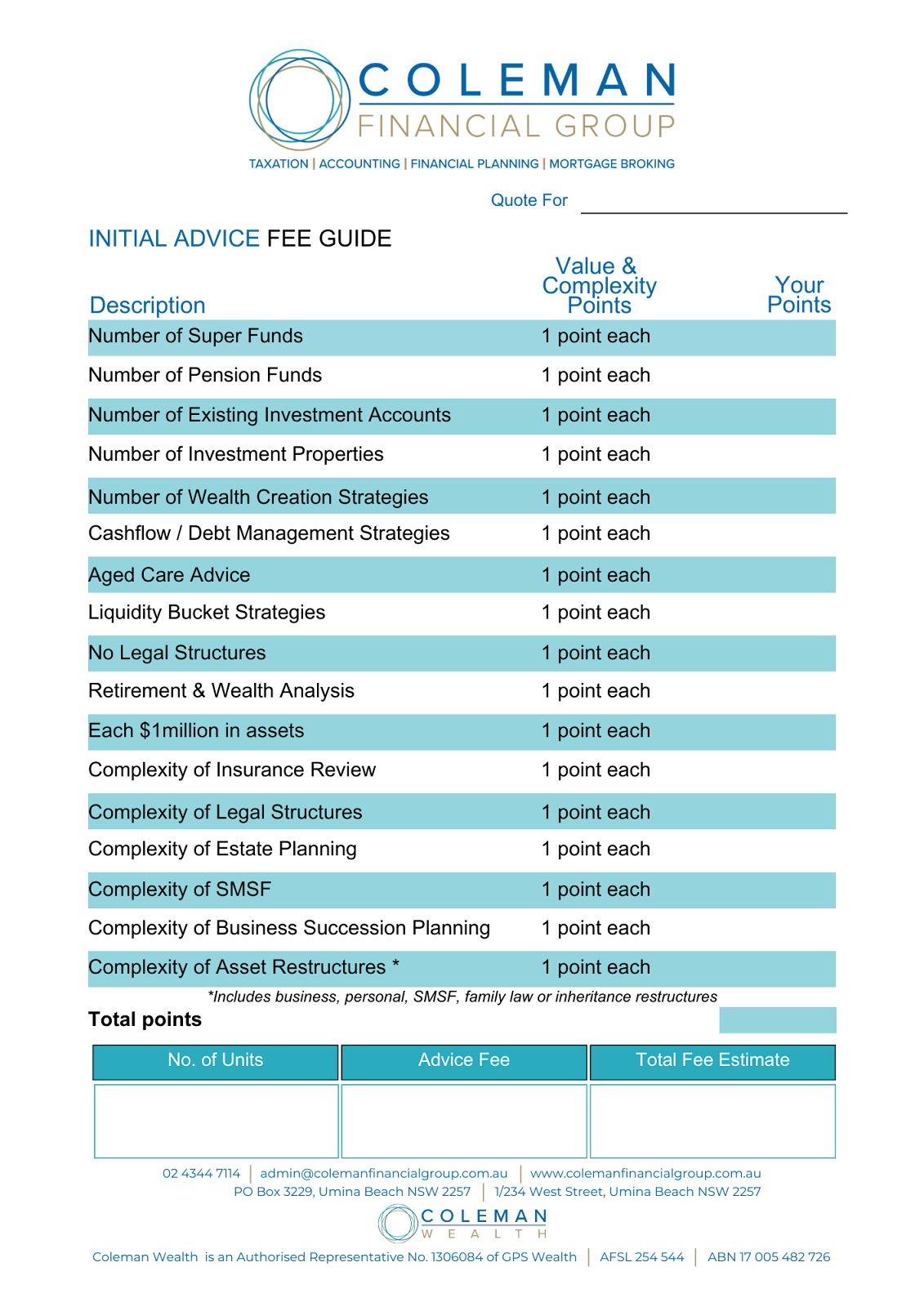

Flat fees provide a straightforward and transparent way to pay for financial advice. Instead of charging based on assets under management or earning commissions from financial products, advisors charge a fixed fee based on the complexity of the service provided.

At Coleman Wealth, we believe flat fees are the fairest payment structure. This approach ensures clients know exactly what they’re paying upfront, with no hidden costs or conflicts of interest. Fees are based on the work required, rather than the size of your portfolio or the products recommended, allowing for truly personalised financial advice.

Coleman Wealth’s Fees

What To Be Aware of When Hiring a Financial advisor

There are a variety of factors you should consider when selecting a financial planner beyond the types of fee structure, this will involve you assessing the person, as well as doing additional research.

The 2026 Education Deadline

As of 1 January 2026, a new law requires all financial advisors to meet strict education and professional standards. Many advisors have left the industry because of these rules, so the ones who remain are the most qualified experts in the field.

The Expertise

What kind of expertise does the advisor have? Do they specialise in a particular area, such as Centrelink financial advice, or navigating the financial aspects of divorce, or do they offer general financial planning services? Understanding their experience and knowledge in your specific financial needs is key to ensuring they can provide the best guidance.

Do they understand you?

You should be able to gauge this from your initial conversation: Do they understand you? Are they actively listening and asking follow-up questions to clarify the important details?

This is one of the most important aspects to consider, as everyone’s financial situation and needs are unique. It’s essential to choose an advisor who takes the time to understand your specific circumstances. Working with a local financial planner can also make communication and face-to-face meetings more convenient.

Check their credibility

It’s also important to verify an advisor’s credibility before making any commitments. A great way to assess their qualifications is by checking the Financial advisor Register, where you can review their education, experience, and any disciplinary history. Sharon Goodwin, our Senior Financial advisor has a master’s degree, whereas many financial planners don’t have this qualification, so it’s crucial to evaluate their expertise beyond just titles.

Additionally, client feedback can offer valuable insights—reviews and recommendations help gauge an advisor’s reputation. For example, Coleman Wealth has over 40 five-star reviews on Google, showcasing our trusted reputation and the satisfaction of our clients. Always take the time to research an advisor’s background and client feedback to ensure you’re working with someone credible and reliable.

How To Get The Best Value

In 2026, new rules will replace the long and confusing “Statement of Advice” with shorter, clearer records. You can get the best value by being open about your finances, which allows your advisor to create the most effective plan for your future.

How Financial Planning Services Affect The Price

The type of services you require plays a significant role in determining the price of financial planning. Whether you’re using a fixed fee or hourly model, the complexity and scope of the services will impact the overall cost. Below are some key factors that influence pricing:

Retirement Planning

Retirement planning is a crucial stage in anyone’s life, and seeking financial advice during this time is essential. Several factors can influence the fees of a retirement financial advisor, such as estate planning, asset management, and income management (like pensions).

While these services can affect the overall cost, they should not deter you. Proper retirement planning is vital to ensure you make the right financial decisions for your future.

Investment Management

Investment management will affect the fees as well. Not all individuals will have investments, and the amount and diversification of investments will also affect the pricing.

Centrelink Advice

Centrelink advice is crucial for individuals navigating the complexities of government benefits and entitlements, especially as they approach retirement or face significant life changes. A financial advisor specialising in Centrelink can help you understand your eligibility for pensions, allowances, and other support programs, and can guide you through strategies to maximise your entitlements. Proper advice ensures you make informed decisions about your financial future, avoiding common pitfalls and potential penalties.

Inheritance

When you inherit assets, it’s important to understand the financial implications. Inheritance advice helps you manage the wealth you receive, whether it’s property, investments, or cash.

A financial advisor can guide you through the process of integrating your inheritance into your overall financial plan, ensuring that tax obligations are met and that you make the most of the assets. They can also help you decide whether to keep, sell, or invest inherited assets, tailoring the approach to your long-term goals.

Divorce and Amicable Separation

Major life transitions, like separation financial advice during divorce often require tailored financial advice. Even when the separation is amicable, dividing assets, managing ongoing obligations, and planning for two independent financial futures can be complex.

A financial advisor can help you navigate these decisions with clarity, ensuring that both parties understand their options and make informed choices around property, superannuation splitting, and long-term planning.

SMSF

Major changes to Self-Managed Super Funds (SMSFs) in 2025 mainly included new limits and thresholds, a higher Superannuation Guarantee (SG) rate, and new rules to follow, such as a proposed tax on balances over $3 million.

Here are the key changes that came into effect from July 1, 2025:

- The Super Guarantee rate increased to 12%.

- The General Transfer Balance Cap increased to $2 million.

- The Concessional Contributions Cap is now $30,000 and the Non-Concessional Cap is $120,000.

Managing your own super fund requires a lot of record-keeping and knowledge of the law. Because of the high standards for 2026, SMSF advice is a specialised service that gives you the most control over your retirement savings.

Multiple Properties

Managing a variety of properties can be a great way to build wealth, but it comes with its own set of complexities.

Having a financial planner means you can be guided on how to structure your investments, assess the potential for growth, and help you balance your property assets with other investment options. Proper advice ensures you optimise the financial benefits of owning multiple properties while minimising risks and tax liabilities.

FAQs

Are financial advisor fees tax-deductible?

Financial adviser fees are generally tax-deductible when they relate to managing existing investments that produce assessable income or for advice concerning tax planning, following the release of Taxation Determination TD 2024/7 in February 2025. While the initial fee for a Statement of Advice was traditionally viewed as a non-deductible capital expense, you can now claim a deduction for the portion specifically related to tax advice. To facilitate this, we provide a separate tax invoice once your strategy is finalised, clearly itemising the proportion that is tax-related for your records. Crucially, ongoing fees are only personally deductible if paid from a personal bank or investment account; if fees are deducted from a superannuation balance, the tax deduction is claimed by the super fund itself and cannot be claimed on your individual tax return.

Is it worth paying for financial advice?

A financial adviser is worth the investment because the long-term financial gain and improved security often far exceed the initial cost of advice. While there is an upfront fee, a professional helps you build wealth more efficiently through the following benefits:

- Strategic Expertise: Managing Australian superannuation, tax laws and government benefits requires specialised knowledge that can significantly improve your net financial position.

- Rational Discipline: An adviser acts as a neutral third party, helping you stick to your long-term plan and preventing emotional decisions during market changes.

- Goal Clarity: Advisers help you set realistic milestones and create a structured roadmap to reach them, whether you are aiming for early retirement or a property purchase.

- Reduced Stress: Most clients find value in the peace of mind that comes from knowing a professional is overseeing their strategy to ensure they stay on track.

- Error Prevention: Professional oversight helps you avoid expensive mistakes in areas like insurance coverage, estate planning and high-fee products.

Can I pay for financial advice using my superannuation?

Yes, you can pay for personal financial advice directly from your superannuation balance under the Delivering Better Financial Outcomes (DBFO) laws. This applies to advice specifically about your super account, such as choosing investment options, making contribution strategies or planning for retirement within your fund. Using your super to cover these costs significantly reduces your out-of-pocket expenses for a comprehensive retirement plan.

What are the new 2026 education standards for advisors?

As of 1 January 2026, all financial advisers on the ASIC Register must meet strict mandatory education standards to continue practicing. Advisers must now hold an approved degree or have qualified through the “experienced provider” pathway, which requires at least 10 years of experience and a clean disciplinary record. These rules ensure that any professional you hire in 2026 meets the highest educational and ethical benchmarks in the history of the Australian industry.

Do I have to pay commissions to a financial advisor?

No, commissions are strictly prohibited in 2026 for all superannuation and investment products to ensure unbiased advice. Commissions are only allowed for life, trauma and income protection insurance policies; however, your adviser cannot accept these without your explicit written consent. Most modern advisers now offer a choice between a commission-based model or a flat-fee service for your insurance needs.

What is the difference between a “Professional Advisor” and the new “Class of Advisor”?

The main difference is that a Professional Financial Adviser provides holistic planning across all your finances, while the New Class of Adviser (NCA) is limited to simple advice on specific products.

- Professional Financial Advisers: Independent experts, like Coleman Financial Group, who provide comprehensive strategies across investments, tax and estate planning.

- New Class of Advisers (NCA): Usually employees of banks or super funds who give basic advice on the products their employer issues. They are legally banned from charging you fees or receiving commissions.